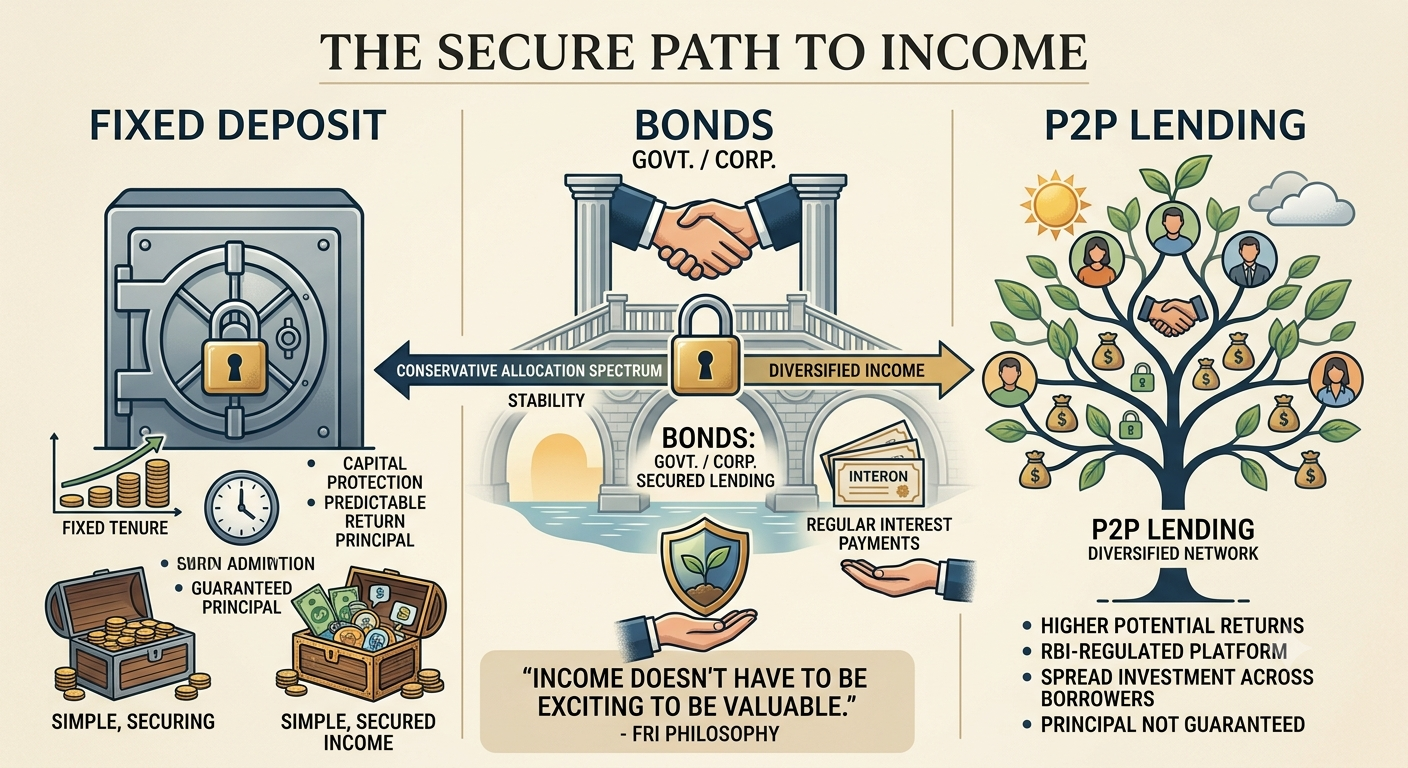

Fixed deposits, bonds, and peer-to-peer lending — the income-generating, capital-preserving side of a portfolio.

Not every rupee in a portfolio is meant to chase growth. Some of it is meant to sit still, generate steady income, and be there exactly when you need it — and there's more than one way to do that, each with a different balance of safety and yield.

Fixed Deposit Fixed deposits don't get much credit for being exciting, and that's precisely the point — a fixed return, for a fixed period, with your principal intact. That predictability matters for money you can't afford to see shrink: an emergency fund, a near-term goal, or the portion of a retiree's portfolio that needs to behave the same way every year, regardless of what markets are doing. We help place FDs with the institutions and tenures that actually match your need, not just the highest rate on offer.

Bonds A bond is essentially a loan — you lend to a government or company for a fixed period and receive regular interest plus your principal back at maturity. Government bonds sit at the safer end of the spectrum; corporate bonds offer higher yields in exchange for taking on the issuer's credit risk. We match the bond's tenure and credit quality to what the money is actually meant to do, rather than chasing the highest yield without asking what risk comes attached to it.

P2P Lending Peer-to-peer lending connects individual lenders directly with verified borrowers through an RBI-regulated NBFC-P2P platform, spreading your investment across many borrowers rather than one loan. It offers the possibility of meaningfully better returns than a traditional FD — but it's important to be clear-eyed: principal is not guaranteed, returns aren't assured, and RBI regulation means the platform follows defined guidelines, not that repayment is backed by the Reserve Bank. It belongs in a portfolio sized to its actual risk, not its advertised return.

"Income doesn't have to be exciting to be valuable."

— FRI Philosophy